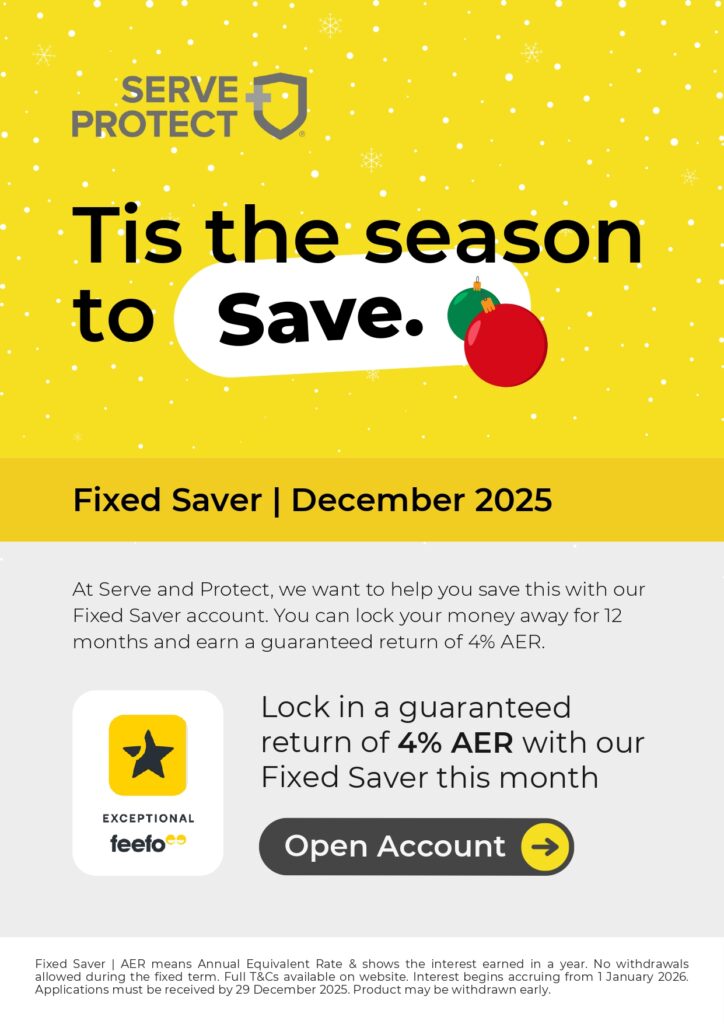

Serve and Protect Credit Union are pleased to announce their latest Fixed-Rate Savings Account.

It’s free to join the credit union and members can open a fixed-rate savings account and lock in a guaranteed rate of 4% AER.

Key details:

✅ 4% AER fixed for 12 months

✅ Balances between £1,000-£10,000

✅No fees or charges

✅Available between 1st to 29th December 2025

If you’d like to learn more about eligibility, terms, or how the account works, please visit: sandpcu.co.uk/fs11

For any questions, please contact Serve and Protect Credit Union

Accord – Free Wills for Police Officers and Staff

Accord Legal Services are offering free wills for all police officers and staff. To arrange your free consultation, call 01744 807048, or email police@accordwills.co.uk.

Police and crime commissioners to be abolished

Police and Crime Commissioner (PCC) roles will be abolished, the Home Office has announced today (13 November)

Reacting to the announcement, chair of the Police Federation of England and Wales (PFEW) Tiff Lynch said: “We welcome this announcement and look forward to helping shape whatever accountability structures replace directly-elected Police and Crime Commissioners.

“We welcome this announcement and look forward to helping shape whatever accountability structures replace directly-elected police and crime commissioners. PCCs were an expensive experiment which has failed.

“The tens of millions of pounds they cost should instead be a down-payment for the sort of policing service this country and its police officers deserve – one with enough officers, with experienced police officers who can afford to keep doing the job, and where officers facing immense stress are properly supported when they put their lives and bodies on the line to protect all of us. The forthcoming Police Reform White Paper is a chance for this government to show it is serious about all of this.

“The Police Federation’s Copped Enough campaign is calling for urgent action to recognise the unique demands of policing, a real plan to keep experienced officers on the beat and protecting our communities with proper recognition of the dangers officers face such as better mental health support.”

Serve and Protect – Free To Access Educational Webinars

To coincide with this week being ‘Talk Money Week’, please see below the links for Serve and Protect latest webinars for November and December 2025.

Register through your personal devices / email addresses should you wish – they do prove quite popular, so it is ‘first come, first served’.

Eco-friendly Ways To Save Money 🌍💸

Eco-friendly savings webinar | November and December 2025 Dates Released | Limited Availability | Learn more and register for FREE

Budgeting 101 📝 📢

Budgeting explained webinar | November and December 2025 Dates Released | Limited Availability | Learn more and register for FREE

Saving Made Simple 💷✅

Tips to boost savings webinar | November and December 2025 Dates Released | Limited Availability | Learn more and register for FREE

Credit Score 101 🚀📊

Tips to boost your score webinar | November and December 2025 Dates Released | Limited Availability | Learn more and register for FREE

Boost Financial Resilience ☔🛡️

Preparing for the unexpected webinar | November and December 2025 Dates Released | Limited Availability | Learn more and register for FREE

Before You Borrow 🔍💸

Key things to know webinar | November and December 2025 Dates Released | Limited Availability | Learn more and register for FREE

Philip Williams – New QR Code

Group Insurance Scheme Members – To ensure you have all the current details of cover and contact details to hand when you need them, add the QR Code to your phone.

How to Add Your PW MemberPass to Your Phone Wallet

- Click the link or scan the QR code below using your phone. Tap “Add to Wallet” when prompted.

- To view full scheme details:

- iPhone: Open Wallet, tap the pass, then tap the (•••) in the top right corner. If you opened Wallet by double-clicking the side button, tap the (i) icon.

- Android: Open the pass and tap “Pass Details”.

From there, you’ll see:

- Scheme Benefits Booklet

- Travel Policy

- Claims Info

- Clickable phone numbers and email links

No need to re-download – your pass updates automatically when we make changes.

No data is collected – your information stays private and secure.

https://wallet.tangent-design.com/install/4d25e327-14c1-0c4e-da83-3a1cb76cedec

Step by Step into Debt Advice

What happens when you contact PayPlan – a step-by-step guide

If you’re thinking about getting support with your finances, but aren’t sure of the process, feel nervous or don’t know what to expect, you’re not alone.

We understand that, for a lot of people, reaching out is often the hardest step, especially when you’re already dealing with stress, uncertainty or the rising cost of living.

To make things easier for you, we’ve put together a step-by-step guide that gives you an idea of what happens when you reach out for our support.

It’s designed to give you a clear picture of:

- how we work

- what you can expect when you contact us

- how we’re able to support you every step of the way on your journey to becoming debt free

Whether you’re just looking at exploring potential options, or know you’re ready to act, we’ll meet you wherever you’re at. This means no fuss and no judgement, just practical solutions you can move forward with at your own pace.

Step 1: Reach out, your way

We’ve got many ways for you to get in touch with us, so you can choose the way that works best for you:

- Call us free on 0800 072 1206

- Live Chat via www.payplan.com/debtadvice

- WhatsApp us here

Step 2: What information will I need to provide?

Whether it’s credit cards, bills or general money worries – we’ll ask a few questions, so we understand the full picture. We’ll ask things like:

- How much you owe

- Who your creditors are

- Your income and expenses

- Any assets you have

Everything you share is confidential and treated with care. We’re here to help, not to judge.

Step 3: Build a simple budget together

We’ll go through your income and spending to understand what’s realistically affordable for you. This includes:

- Wages, benefits, bills, travel and childcare

- Grocery and living costs

- Subscriptions and day-to-day spending

This helps us to work out what’s affordable for you and what kind of debt solution could work best for you.

We know that talking about money can feel uncomfortable, but it’s important to be as open and accurate as you can.

Step 4: Explore suitable options

At this point, we should have a complete picture of your situation, and we can talk you through the options available to you. We’ll walk you through:

- What each option means

- How it works day-to-day

- Any fees or next steps

- What’s best suited to you

We’ll give you space to think, ask questions and make decisions at your own pace.

Step 5: Decide how you want to move forward

Once we’ve talked through your options, we’ll help you choose the right next step – whether that’s a managed plan or another type of support.

Some people go ahead with a plan that we manage for them. Others may be better suited to a different kind of solution, like either insolvency, debt relief orders (DROs), repayment arrangements (RAs), bankruptcy, or depending on where in the UK you are, one of our Scottish solutions. Whatever your path, we’ll guide you through it.

Here’s what that might look like:

- If you’re opting for a Debt Management Plan (DMP), we can manage this in-house. Our friendly advisors will walk you through each step and keep you supported throughout.

- If you’re entering an into an insolvency agreement, we’ll refer to our specialist teams:

- PayPlan Partnership Limited for non-self-employed Individual Voluntary Arrangements (IVAs)

- PayPlan Bespoke Solutions Limited if you’re self-employed

- If you’re in one of our Scottish solutions, you’ll be supported by PayPlan Scotland – they’re experts in whichever solution you choose.

Once you’ve made a decision, we’ll get everything set up. Most of the time, we’ll contact you by phone, email or WhatsApp – whichever suits you best.

And even if your solution isn’t something we manage directly, we’ll still be here to guide and support you through it.

What you can do next

If you are struggling with debts call us on 0800 072 1206. We’re open from 8am – 8pm Monday to Friday and 9am – 3pm on Saturdays.

Alternatively, you can visit our www.payplan.com/police to speak to us via live chat or for more information.

Free Webinar on the 1987 Police Pension Scheme

Free Financial Resilience Webinar from Serve and Protect Credit Union on the 1987 Police Pension Scheme

Webinar Dates

- Monday 3 November 2025 (12:00-13:30)

- Monday 17 November 2025 (12:00-13:30)

- Monday 08 December 2025 (12:00-13:30)

Simply click on the link above and choose the session from the drop-down menu that you’d like to attend, then join us online, totally free with no commitment.

Food Inflation in the UK

What’s driving food inflation and how you can save on your food bill

Food inflation within the UK has increased again, rising 4.9% year-on-year in July 2025, marking the highest rate since February 2024. Over the past five years, food prices have climbed by an average of 37%, with some staples seeing even sharper increases. [1]

Many households are being stretched already by rising energy prices and other costs which are increasing pressure on household budgets.

What’s causing the rise?

- Global raw material price increases. For example, chocolate has experienced the most dramatic price increases of any major food category. Prices are up by 16% in the past year alone, with cumulative inflation reaching 43% since 2022. [2]

- Increases in National Insurance contributions and the minimum wage rise have impacted what food retailers are charging for food to cover their costs.

- Increased production and transportation costs.

- Currency fluctuations.

How to save money on your food shopping

Whilst inflation is out of your control, there are some practical steps you can take to reduce your food shopping bill.

- Plan your meals for the week and shop with a list to help avoid impulse buys.

- Buy in bulk if there’s a particularly good deal on a product you’ll use. Check dates as some offers have short shelf lives.

- Use supermarket own brand products – they can often be significantly cheaper.

- Make the most out of loyalty schemes for supermarkets and cashback apps to earn rewards on your weekly shop.

- Try BudgetSmart, our free tool to help find savings and improve your financial confidence.

Reduce food waste to save having to rebuy

- Store your food shopping correctly to extend shelf life.

- Make the most of leftovers – you can create soups, casseroles and stirfries which can be great ways to use up left over bits of food.

- Organise your cupboards by use by date order to avoid wastage.

If you’re struggling with the rising cost of your food shopping you’re not alone

If you are struggling with debts call us on 0800 072 1206. We’re open from 8am – 8pm Monday to Friday and 9am – 3pm on Saturdays.

Alternatively, you can visit our www.payplan.com/police to speak to us via live chat or for more information.

[1] UK inflation rises by more than expected to 3.8%, largely driven by air fares – BBC News

[2] Why are food prices rising in the UK? – Economics Observatory

Police Insure – One4all Gift Card

New Police Insure offer – if they can’t beat your existing provider’s renewal premium, they’ll give you a £50 One4all Gift Card.